Under the powerful wave of AI, the global memory market is experiencing an unprecedented structural supply and demand imbalance. Among them, the shortage crisis of DRAM (dynamic random access memory) has escalated from a market warning to a "fo...

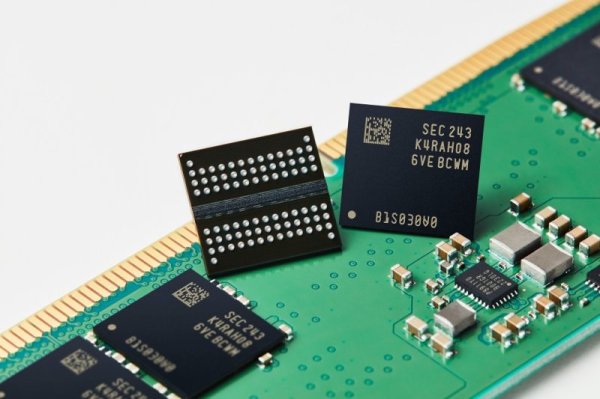

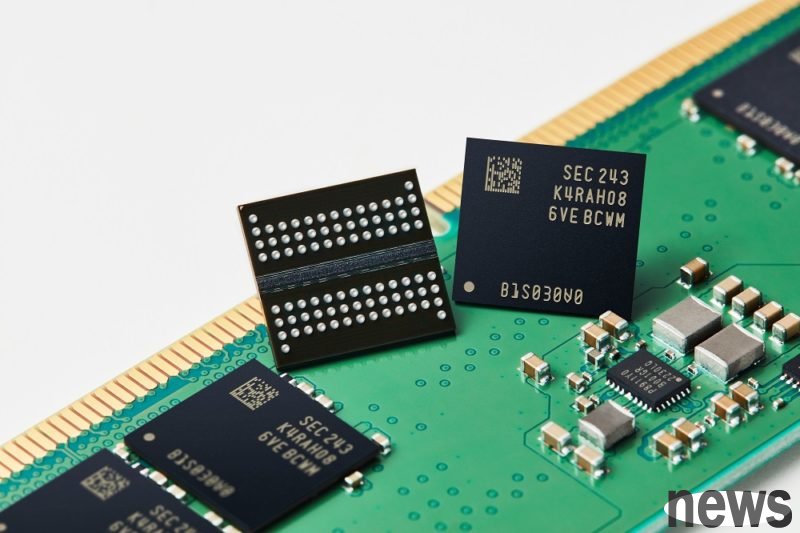

Under the powerful wave of AI, the global memory market is experiencing an unprecedented structural supply and demand imbalance. Among them, the shortage crisis of DRAM (dynamic random access memory) has escalated from a market warning to a "food shortage" panic in the supply chain. The core event of this crisis is that memory leader Samsung Electronics took the lead in suspending contract quotations for DDR5 DRAM in October. This move immediately triggered other original manufacturers such as SK Hynix and Micron to follow suit, causing the supply chain to face severe supply interruptions, forcing companies in urgent need to turn to the spot market to grab goods.

Digitimes reported that the intensification of the memory shortage is mainly due to the continued expansion of capital expenditures by cloud service providers (CSPs) and the increasingly serious crowding out effect of AI computing. Against the background of the original factory's tightening supply strategy, Samsung delayed providing contract quotations in October and even told downstream customers that it had "no stock to sell." This move directly caused the DDR5 spot price to increase by 25% in just one week.

Market research and survey unit TrendForce stated that there are currently quotations in the market, but they are indeed passive, resulting in very limited transactions in October, and prices have also changed from a single-quarter model to monthly quotations. Judging from the current quotation situation, Samsung has mainly suspended quotations, and other suppliers have also turned to a wait-and-see attitude, creating a bidding atmosphere. Industry insiders are worried that original manufacturers not providing quotations may become the norm in the future. Since the upstream original manufacturers currently only provide quotations for major technology manufacturers or first-tier CSP companies, DDR5 is almost not released to other general customers. This supply crunch has made the memory market completely enter a "seller's market."

Due to the suspension of contract quotations, the spot market became the only option, causing prices to soar rapidly. DRAM spot prices have experienced a crazy rise in the past month. Among them, the price of DDR5 16Gb has soared from US$7.68 at the end of September to US$15.5 in a single month, an increase of 102% in a single month, making it the most astonishing price increase among all product lines. In addition, although the contract price for the fourth quarter has not yet been confirmed, the market expects that from the fourth quarter to the first half of 2026, DDR5 prices will show a skyrocketing trend, with double-digit increases quarter by quarter. If the trend continues, DDR5 16Gb prices may reach as high as US$30 in the first half of 2026.

The crisis triggered by the suspension of quotations for DDR5, Gou Jiazhang, general manager of memory control IC manufacturer Huirong, analyzed that this round of shortage is different from the past. It is not caused by a single factor or production reduction. It involves multiple core components being out of stock at the same time, forming a strong "pull" demand.

Gou Jiazhang emphasized that the fundamental shortage comes from the explosive growth in demand for artificial intelligence inference (AI Inference), which has caused an extreme squeeze effect on HBM. Currently, memory and storage components are in extremely short supply, and HBM is out of stock. In addition to NVIDIA (NVIDIA), the demand for GPUs and accelerators from major manufacturers such as AMD, Broadcom, Microsoft, Google, Meta, and Amazon has also increased simultaneously. Even the demand for HBM in the Chinese market is also increasing.

In addition, production capacity is structurally limited. Under strong demand for HBM, major DRAM manufacturers are shifting capital expenditures and production capacity to more profitable DDR5 and HBM production, resulting in tight overall DRAM production capacity. Gou Jiazhang pointed out that there are serious structural constraints in HBM production. Because to achieve the same density as DDR5, HBM requires up to three times the wafer output. This transition has significantly squeezed out the supply space of traditional DRAM.

Gou Jiazhang also observed that capital expenditures in the AI field are undergoing a key shift. While AI training is still growing, capex for AI inference is expected to significantly exceed training by 2026. AI inference has extremely huge demands on memory and storage, placing strong demands on HBM, high-capacity SSD and hard disk drive (HDD). Therefore, under the structural shortage, DRAM supply is no longer tight as originally expected. In particular, the current market gap is no longer 70% to 80% of the original expectation, but the gap between demand and output has doubled.

This "panic shortage" directly changed the industry's bargaining model. Gou Jiazhang emphasized that the focus of bargaining has shifted from "price" to "supply capacity," which has resulted in the suspension of DDR5 DRAM contract quotations. Under this situation, even major technology companies such as Apple are working hard to allocate production capacity in 2026, and they may not be able to get the full amount. This shows that the market has entered the "as long as the goods are available" stage, and price negotiations have almost come to a standstill.

Also, the four major CSP players in the United States (Amazon, Google, Meta, and Microsoft) have all recently revised up their capital expenditures, and are expected to increase investment in 2026. This strong demand for high-end memory chips continues unabated, causing original manufacturers to shift production capacity to higher-profit DDR5 and HBM products in pursuit of higher profit margins. Furthermore, adding capacity for advanced DDR technologies such as DDR5 is expensive and time-consuming. To increase DDR capacity by ten thousand wafers per month using 1b or 1c technology, the required advanced technology capital expenditures would be approximately $10 billion. Due to the long delivery time of advanced equipment and complex manufacturing processes, production capacity cannot be increased rapidly, making it difficult to alleviate the gap between supply and demand in the short term..

Based on the above situation, the world's three major memory manufacturers, including Samsung, SK Hynix, and Micron, are unable to provide enough DRAM for this wave of AI demand. Therefore, major manufacturers are actively investing in the R&D and mass production of HBM. Among them, SK Hynix expects that by 2027, when its large-scale FAP begins mass production of DRAM, the DRAM shortage situation can be alleviated to a certain extent. Samsung expects to reach a considerable level of HBM production capacity by the end of 2026. Micron is accelerating the expansion of production capacity at its HPN (HBM) plant in Singapore.

However, in the face of the suspension of quotations by original manufacturers, module manufacturers are generally worried that "after food is cut off, they will only become hungrier." Under the expectation that prices will continue to rise, purchase costs are in a dilemma. Gou Jiazhang also previously predicted that the current structural shortage will continue until 2026. As for the situation in 2027, it is still impossible to predict. The key turning point is when the situation of repeated orders begins to ferment. Therefore, this structural shortage driven by AI is testing the corporate responsibility of major DRAM manufacturers. They face the daunting challenge of balancing resource allocation between their lucrative data center needs and other industry chains such as mobile phones and automobiles. Otherwise, it may lead to the collapse of the entire industry chain.

All in all, Samsung’s suspension of DDR5 contract quotations is the epitome of the extreme imbalance between supply and demand in the memory market under the current AI craze. Due to the structural limitations of HBM's production capacity and the explosion of demand for high-performance memory due to AI inference, the supply of DDR5, which was supposed to be a mainstream product, has been extremely compressed, causing prices to double in a single month and pushing the market completely into a seller's market. This change, caused by the overlap of structural restrictions and unprecedented strong demand, will continue to test the wisdom and response capabilities of major manufacturers.